Shipping and Freight Review 2019

The last year of the decade is fast fading into the horizon.. 2019 is almost done..

Personally for me, this means I have been a part of this dynamic industry now for

30 years =

10,950 days =

262,800 hours =

15,768,000 minutes =

946,080,000 seconds and counting

Wow, time does fly when you are having fun………!!!!“..

But I am loving it and would not have it any other way.. But more importantly, I am glad to have shared the last 10 years of this time interacting with YOU, my readers and my constant and ardent supporters and well wishers.. 🙂

Here is my review of how the shipping and freight industry fared in 2019 and the decade..

Trade in 2019

WTO (World Trade Organisation) reported that world exports and imports contracted by 2.7% and 3.1% respectively year on year in the 1st quarter of 2019..

The WTO had to sharply lower their forecasts for trade growth in 2019 and 2020 on the back of escalating trade tensions and a slowing global economy..

They estimate that the merchandise trade volume growth will fall to 2.6% in 2019 — down from 3.0% in 2018 but expect it to rebound to 3.0% in 2020 provided of course the trade tensions ease up..

Source : WTO

Source : WTO

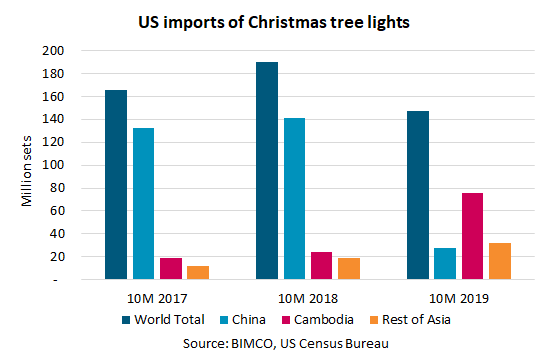

The effect of the trade wars are being felt in many areas and commodities, not just in major traded commodities, but even in seasonal commodities such as Christmas tree lighting sets..

As per reports, USA imported just 27 million sets of Christmas tree lighting sets from China in 2019 compared to 140 million sets in 2018.. This as a direct result of the trade wars..

But what is one person’s loss is another person’s gain with other countries in the region filling this gap.. In this case, China’s loss was Cambodia’s gain..

As per OECD reports, the G20 international merchandise trade saw a downward trend in the third quarter of 2019, which is close to two-year lows.. In total within the G20 countries, exports contracted by 0.7% and imports by 0.9% compared with the second quarter of 2019..

The slowdown was quite marked in all the major regions as shown below..

Source : OECD

Source : OECD

Maritime trade growth was down in 2018/2019 on the back of softer economic indicators, heightened uncertainty and wide-ranging downside risks as per UNCTAD statistics.. This downturn naturally resulted in port traffic growth also going down..

According to UNCTAD projections, international maritime trade will increase by 2.6 per cent in 2019 and will continue rising at a compound annual growth rate of 3.4 per cent over the 2019–2024 period..

However this could be affected due to below key factors..

Environmental concerns such as air pollution, climate change and fuel economics;

Geo political concerns such as US/China trade tensions, Strait of Hormuz being used as a strategic maritime chokepoint;

Shifts in globalization patterns

Shipping and Freight review for the decade (2010-2019)

While there have been many talking points relating to the industry in this decade, a few significant points which stand out for me from this decade are :

The race to be the biggest container ship in the world

Consolidation and alliances of container shipping lines

Tackling climate change in shipping

Recurring maritime disasters which has brought a sharp focus on safety and compliance in the industry

The impact of digitalisation in the shipping and freight industry

Mirror, Mirror on the wall, Who is the biggest of them all..??

2013 saw the arrival of the first Triple E vessels by Maersk which probably kick started the “size race” with ships displacing each other in quick succession to gain the title of “biggest container ship in the world“..

From 2013 till now, 8 ships have laid claim to this title..

After a lull between 2017 and 2019, there seems to be a renewed drive for these ULCVs with a reported 50 ULCVs on order between now and 2022..

90% of shipbuilding activities were done in shipyards based in China (40%), South Korea (25%) and Japan (25%) with China accounting for a whopping 49% of container ship deliveries..

It is reported that these 50 ULCVs will bring in an additional capacity of 1,093,442 TEUs into the global container capacity, adding to the 108 ULCVs already in service with a 2,131,043 TEU capacity..

Probably on the back of this battle and to ensure survival, there was a scramble by the lines to sustain themselves through consolidation, mergers and acquisitions and alliances..

Mergers, Acquisitions, Consolidation and Demise

Below were some of the significant Mergers, Acquisitions, Consolidation and Demise within the container shipping industry that shaped this decade and probably influencing the container shipping sector of the future..

Hanjin Shipping the 4th largest container operator in 2000 was declared bankrupt and shut shop in 2016.. Hanjin was the 7th largest container shipping line at the time of its demise, the first time a container line in the Top 10 went bust in the history of shipping, sending shock waves and a clear message to the other carriers;

Hapag Lloyd‘s merger with CSAV & UASC the 16th ,17th and 22nd largest container operators respectively in 2000, made them the 5th largest container operator in the world in 2019;

Cosco Shipping Lines Co Ltd, leap frogged from its position of 7th largest container operator in the world in 2000 to the position of 3rd largest container operator in the world in 2019 with its merger with China Shipping and its take over of OOCL;

CMA-CGM’s take over of NOL which included APL – 6th largest container operator in 2000, made them the 4th largest container operator in the world in 2019;

Maersk’s acquisition of Hamburg Sud the 20th largest container operator in 2000 added to its already strong position in the list as the largest container operator in the world;

Then 3 became ONE (Ocean Network Express) when the Japanese container carriers K-Line, MOL and NYK Line’s merged making them the 6th largest container operator in the world

All these M&As has changed the dynamics of the container shipping industry and its outlook from what it was in 2000..

In the year 2000, out of the Top 100 container lines, the top 25 had an 81% market share of which, the top 10 only had a 52% market share..

Fast forward to the end of this decade in 2019, out of the Top 100 container lines, the top 25 have a market share of 91.20% of which, the top 10 have a whopping 83.40% market share..

This drastic change can be attributed mainly due to the Mergers & Acquisitions that have taken place in the shipping industry in this decade..

On top of these Mergers & Acquisitions, this decade also saw the creation of alliances between container shipping lines

2M consisting of Maersk (1), MSC (2), ZIM (11) accounts for 34.80% share in the Top 100 container shipping lines

Ocean Alliance consisting of CMA-CGM (4), Cosco (3), Evergreen (7) accounts for 29.60% share in the Top 100 container shipping lines

THE Alliance consisting of Hapag-Lloyd (5), ONE (6), YML (8) accounts for 18.40% share in the Top 100 container shipping lines

These 3 alliances together total 82.80% of the Top 100 container shipping lines in the world, leaving about 17.20% of those lines not part of any alliances

Below is a representation of the Top 100 container shipping lines in the world and market share by alliance..

Freight forwarders have also been having their own share of M&As, but in relation to shipping lines, the big ones will be the acquisition of Ceva Logistics by CMA CGM and with Maersk acquiring Vandegrift expanding their footprint and converting their business to an Integrated Logistics Services Provider including customs clearance and freight forwarding..

Combating Climate Change and Cost Impact of IMO 2020

Although the shipping industry has one of the lowest carbon emissions compared to other modes of transport, climate change and reduction of GHG emissions from ships has been foremost in the minds of the shipping community..

The International Maritime Organization (IMO) which is the regulatory authority for international shipping, has been working to reduce the harmful impacts of shipping on the environment since the 1960s..

The regulations for the Prevention of Air Pollution from Ships (Annex VI) seek to control airborne emissions from ships (sulphur oxides (SOx), nitrogen oxides (NOx), ozone-depleting substances (ODS), volatile organic compounds (VOC) and shipboard incineration) and their contribution to local and global air pollution, human health issues and environmental problems..

In 2016, at the 70th session of the Marine Environment Protection Committee (MEPC) meeting in London, the International Maritime Organization (IMO) took a landmark decision setting 1st January 2020 (colloquially known as IMO 2020) as the implementation date for a significant reduction in the sulphur content of the fuel oil used by ships..

What this means is that from the 1st of January 2020, all commercial ships can only use marine fuels with the new global sulphur limit of 0.50%..

Ship owners have a few options to ensure compliance of above and meet lower sulphur emission standards, each with some pros and cons..

Using Low Sulphur Fuel

Using LNG to power the ships

Using Scrubbers to clean emissions before they are leased into the atmosphere

Cost Impact of IMO 2020

Each method has its own pros and cons and naturally such compliance requirements bring along with it additional costs and uncertainty in terms of fuel costs for shipping lines and customers..

Carriers will be exposed to huge costs in preparing the ships to meet the required standards of IMO 2020..

MSC estimates that the cost of the various changes that will need to be made to their fleet and its fuel supply is in excess of two billion dollars (USD) per year while Maersk Line expects its extra fuel and compliance costs to exceed USD 2 billion..

Hapag Lloyd’s CEO mentioned that they are expecting their low sulfur fuel costs to be around USD75-100 million during the 4th Quarter of 2019 in order to be ready for IMO 2020 implementation date of Jan 1, 2020..

Many shipping lines like CMA-CGM, ONE, OOCL and APL had announced that the costs for compliance will have to be passed on to customers/trade and this will be done through the implementation of new or adjustment to existing fuel surcharges, which may vary based on the trade lanes..

The shipping lines have advised that they are not going to pay for these costs alone as environmental protection is everyone’s baby and have also made their intentions clear by implementing additional surcharges to cover for these extra costs that they will be incurring to operate their ships on cleaner fuel..

So naturally either the seller or buyer will have to foot the bill for these additional surcharges.. Now, more than ever the sellers and buyers need to ensure that their contract of sale is carefully worded around these costs and the correct Incoterms® is used..

Maritime & Related Disasters

The maritime industry is said to have one of the worst safety performances of any industry and the maritime disasters that happened in 2019 and this decade lends credence to this.. The serious maritime disasters in this decade were :

2012 – MSC Flaminia went up in flames between USA to Europe apparently due to lack of proper communication relating to carriage of hazardous goods.. The shipper and tank operator were held liable..

2015 – More than 112 people were killed in a hazardous goods explosion in a container storage yard in Tianjin..

2018 – Maersk Honam, one of Maersk’s ultra-large containership caught fire while en-route from Singapore to Egypt, in the Arabian Sea in which five crew members perished..

2019 – MSC Zoe, a 396m long containership capable of carrying 19,224 TEU lost as much as 270 odd containers which went overboard in tough weather conditions..

2019 – Yantian Express, a 7,510 TEU, 320m German-flagged ship of Hapag Lloyd went up in flames while on its way from Colombo to Halifax via the Suez Canal..

2019 – KMTC Hong Kong catches on fire at the Laem Chabang port in Thailand possibly due to undeclared hazardous containers on board..

These were just some of the incidents.. As per the European Maritime Safety Agency, in this decade, between the period 2011-2018 below were the statistics of maritime disasters..

Source : European Maritime Safety Agency

Source : European Maritime Safety Agency

Navigating the sea of digitalisation

This decade will also be remembered as the decade that spawned several hundreds of startups in the shipping and freight industry including self-proclaimed digital freight forwarders some of whom have been evaluated to be worth $3.2 billion and have received funding of upto $1 billion in venture capital for the first time in the history of this industry..

Shipping lines have also formed their own digital alliances with the likes of Maersk and IBM teaming up to create Tradelens to offer customers digital freight solutions.. As per Tradelens, they are an open and neutral industry platform underpinned by Blockchain technology, supported by major industry players such as Maersk, Zim Lines, PIL, CMA CGM, MSC, Hapag Lloyd and ONE..

Maersk, Hapag Lloyd, MSC, ONE, created Digital Container Shipping Association which was later joined by CMA CGM, Evergreen Line, Hyundai Merchant Marine, Yang Ming, and ZIM.. DCSA’s major initiative is said to be on moving the shipping and freight industry away from a silo approach of individual standardization and getting the industry players to work together on enhancing industry-wide information technology standards..

In keeping up with this intiative, DCSA have announced the first Container Shipping Industry Blueprint ‘IBP 1.0’ which contains the recommended current state standards for the processes used in container shipping, as seen from the carrier’s perspective..

DCSA and its founding members: Maersk, CMA CGM, Hapag-Lloyd, MSC and ONE have mapped the processes commonly used in container shipping from Carrier Booking to Container Return to create a common view across the industry..

The hope and ambition is that the carriers will start using this standard and align their businesses to it when delivering further digitalisation and standardization initiatives in the industry in the future..

This decade also saw several exciting developments in the world of digitalisation of the shipping industry including blockchain..

Blockchain seems to have become a prolific “enabler” of businesses, particularly in the shipping and freight and trade industry.. Whether it is

blockchain is making its presence felt quite rapidly in our industry..

Many shipping lines, ports, financial institutions and other private entities are using Blockchain and testing it in many different ways through many pilot projects..

Shipping and Freight Resource

This decade saw Shipping and Freight Resource celebrating a decennary, a decennium, a decade or in simple English, 10 years of helping people to Seek » Learn » Know » Grow in the shipping and freight industry having been viewed over 11.5 million times by over 6.1 million visitors..

The below are the Top 10 articles of my site based on reader visits.. Like a Radio Top 40 scenario, you are the ones who can add to or change this list of your favourite articles on the site.. You can view this post by post list to see other articles/topics of interest to you..

What is a HS Code..??

Difference between House bill of lading and Master bill of lading

Difference between Demurrage and Detention

How to calculate CBM and Freight Ton

Difference between a Liner and Tramp service

What is a Switch Bill of Lading and when and why is it used..??

Difference between a Freight Forwarder and NVOCC

What is CY-CY Term in Container Shipping..??

How does demurrage, detention and port charges work..??

Shipping Jargon

Below however is my personal Top 10 articles from among the hundreds of articles on this site..

Difference between Maritime, Shipping, Freight, Logistics and Supply Chain

Vintage Shipping – the way it was done

What is a Bill of Lading..??

How does demurrage, detention and port charges work..??

8 points to consider before you sign a bill of lading

6 points to help you compete in the shipping and freight industry

Do I need cargo insurance for my shipment

Causes of Demurrage and Detention

Parts of a Bill of Lading

When does a Bill of Lading become a Contract of Carriage

As I have mentioned previously, while it is an honor that this resource is being visited by readers from some of the main maritime centers of the world such as Singapore, UK, India and UAE, which form part of the Top 10 countries visiting my blog, I am equally honored to receive visitors from some of the remote countries like Guernsey, Åland Islands, Wallis & Futuna, St.Pierre & Miquelon and many more..

WISH EVERYONE A HAPPY AND SAFE HOLIDAYS, THE BEST OF HEALTH, WEALTH, HAPPINESS AND PROSPERITY IN 2020,and of courseWORLD PEACE.. 🙂

Like this:

Like Loading…

Write a Comment